- (+27) 72 578 1433

- info@wealth-bridge.co.za

- Follow Us :

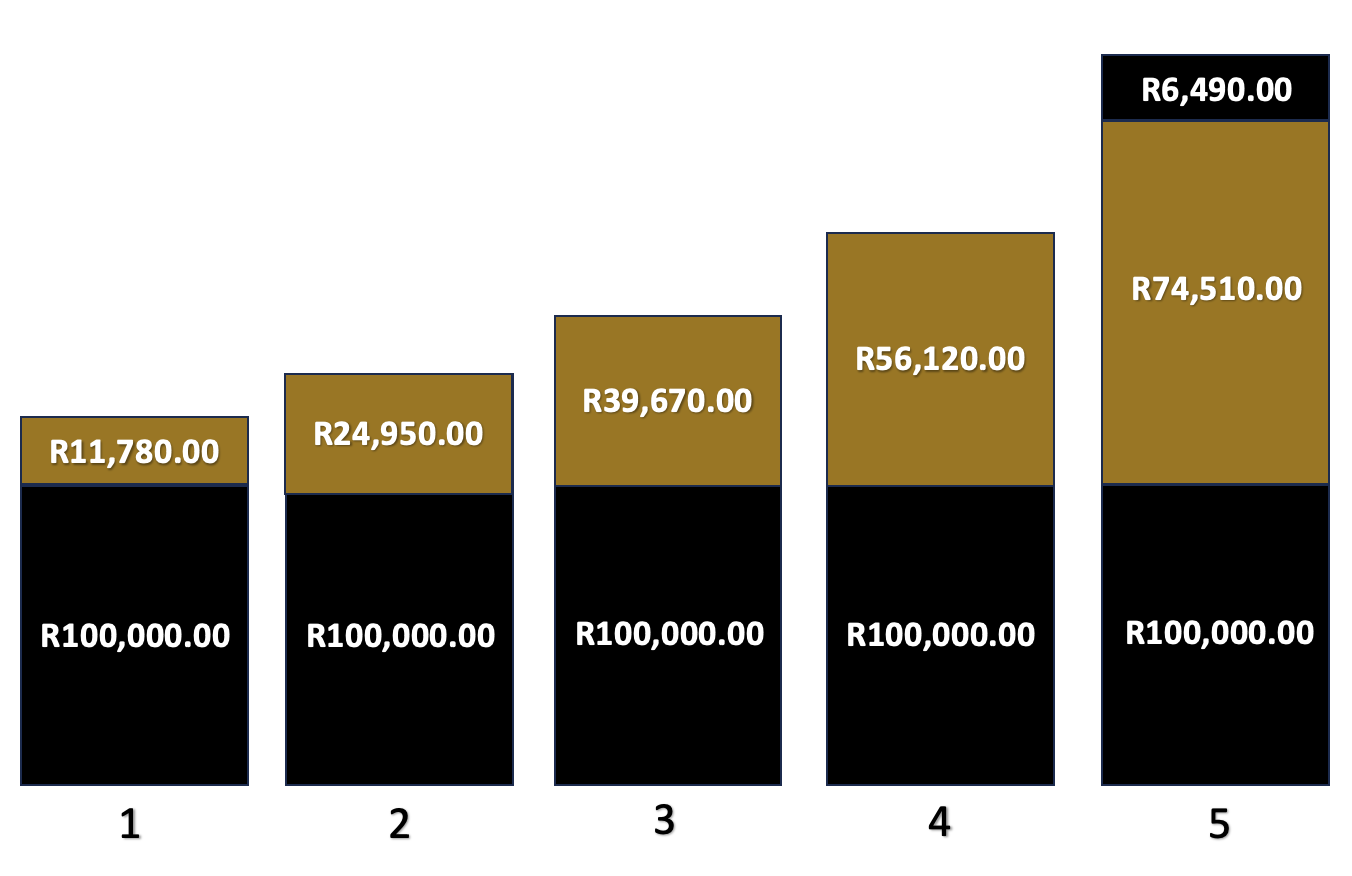

Minimum investment: R 100 000

Yield: Compounding 11.78% over 5 years added with up to 6.49% boost if invested for the full term.

Investment term: 5 years

Notice period after lock-in term: 3 months

Diversification factor: Investment is diversified over more than 10 companies in 10 different sectors

The boost: A boost of up to 6.49% can be expected if invested in the growth option for 5 years. If the switch is made after year 4 the boost is up to 3.25%. If the switch is made after year 3 the boost is up to 1.62%. If the switch is made before 3 years the boost will be forfeited. The boost is not a guarantee and is based on investment performance.

Penalties: There is a 10% penalty if the investment is withdrawn within the first year, from year 2 the penalty is 5% until the investment has reached maturity.

*No yields are payable from withdrawal instruction.

Investment gains (excluding local dividends) will be subject to your applicable rate of income tax. nReach Capitis Laysan (Pty) Ltd will issue you with an investment statement for this purpose. It is your responsibility to pay the applicable taxes on these gains on your Select Portfolio.

Capital gain refers to an increase in a capital asset's value and is considered to be realized when the asset is sold. If an investment is left without a withdrawal of interest for longer than 36 months, the investment is taxed on the Capital gains tax model and not the Income tax structure. The client is responsible for any tax liable to SARS.

The gross investment return will depend on financial market conditions and the rate of inflation during the policy term. Inflation has a major impact on investment returns, and in general higher inflation leads to higher investment returns and lower inflation leads to lower investment returns. Real rates of return (the excess of the investment return over the inflation rate) gives a more meaningful indication of how the investment has performed.

Boost

The boost vests at the end of the investment term up to 6.49% if the investment is invested in the growth option for 5 years. If withdrawn after year 4 the boost is up to 3.25%. If withdrawn after the year 3 the boost is up to 1.62%. If withdrawn before 3 years the boost will be forfeited. The boost is not a guarantee and is based on investment performance.

Due to the contracted yield no admin, performance management fees, commissions and platform fees may be deducted if the contracted yield is not met. All the fees mentioned above is payable by the fund manager.

This option is designed with capital growth in mind. From inception there is a 3 calendar month notice period. The product has a 60 month term. After the term, the investment will be paid out to the client. Penalty for early withdrawal will be 10% of investment value in the first year of the product term. From year 2 the penalty gets reduced to 5% until the investment has reached the full term. No yield is payable from notice date instruction. If the investment is larger than five million rand, only five million rand can be withdrawn at a time. As soon as the first five million rand has been paid, the notice for the remainder can be submitted where the same withdrawal rules apply.

In the event of your death, the net value of your investment fund will be payable to your estate and distributed according to the wishes in your will or the law.